Sulphuric acid is a foundational industrial chemical for, e.g., phosphate fertiliser, mining and several clean-tech supply chains.

For decades, supply was reliable, abundant, and cheap, a byproduct of fossil fuel refining that the world generated almost automatically. Because much of the world’s sulfur comes from fossil-fuel refining and smelter byproducts, the transition away from fossil fuels and recent market disruptions have made supply security and circular alternatives more strategically important, bringing forward domestic circular alternatives.

The Geography of Dependency

Approximately 90% of the world’s sulphur is recovered as a byproduct of oil refining and natural gas processing, mandated by environmental regulation to prevent toxic sulphur dioxide emissions. [19]

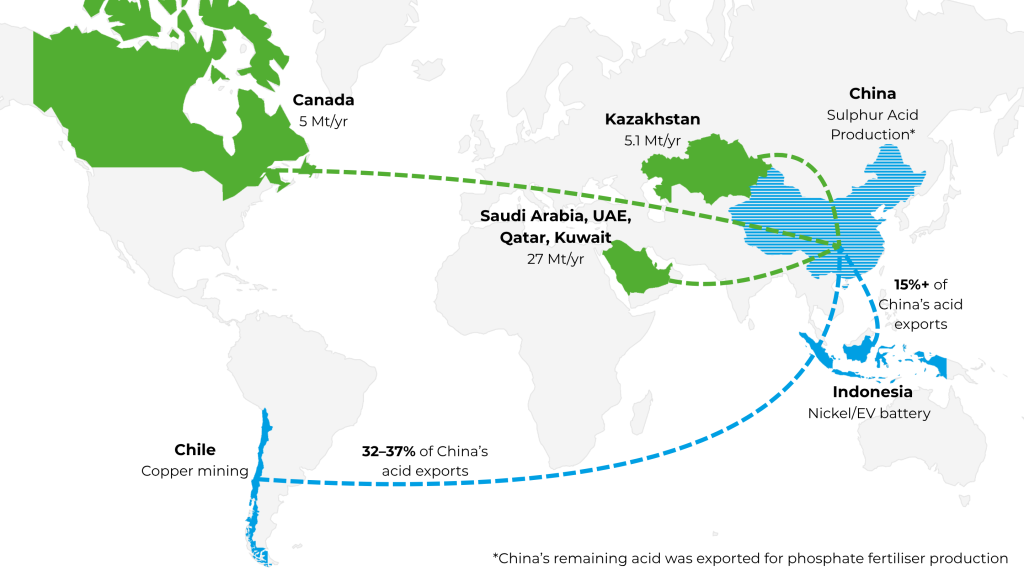

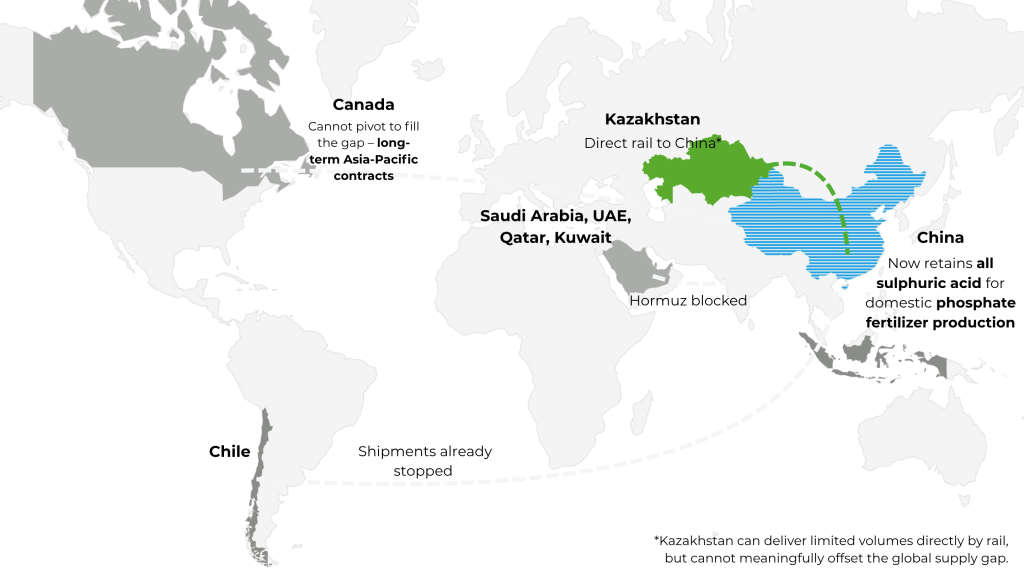

The Middle East is the undisputed hub. Saudi Arabia, the UAE, Qatar, and Kuwait collectively account for roughly one-third of global sulphur production and approximately 50% of the seaborne trade. [13] Kazakhstan has emerged as a critical secondary node, the single largest sulphur exporting country globally in 2024, shipping over 5 million metric tonnes, but its export corridor runs through Russian rail and port infrastructure, a route that has grown increasingly precarious under geopolitical pressure. [15] Canada produces a comparable volume (~5 million tonnes annually), but its long-term contracts are oriented toward Asia-Pacific markets and cannot offset a Middle Eastern deficit. [5]

China occupies a pivotal position in the value chain: the world’s largest importer of elemental sulphur and, simultaneously, the world’s largest producer and exporter of byproduct sulphuric acid. [16]

Hormuz, Russia, Beijing: When All Three Break at Once

The escalation of conflict in the Middle East from late February 2026 onward has compromised transit through the Strait of Hormuz, trapping millions of tonnes of sulphur supply available in the seaborne market. Russia has extended its temporary ban on industrial sulphur exports, a measure originally introduced to protect domestic supply.[18]

On April 10, 2026, China’s National Development and Reform Commission notified domestic producers of a comprehensive halt on sulphuric acid exports, effective May 1. [4] The stated rationale was national food security: by restricting acid exports, Beijing aimed to depress domestic acid prices and reduce production costs for Chinese phosphate fertiliser producers. Shipments to Chile, which absorbed nearly one-third of China’s overseas acid exports in 2025, ceased entirely in April for the first time since July 2023. [6]

The Downstream Exposure

Fertilisers

The fertiliser industry accounts for approximately 54% of global sulphuric acid demand. [14] Major global companies like OCP Group, The Mosaic Company, and Nutrien Ltd. use sulphuric acid to digest phosphate rock into phosphoric acid, the precursor for the most widely applied phosphorus fertilisers globally. [10] [17] [11]

A sustained shortage of sulphuric acid directly impacts food production costs and agricultural supply chains, which is precisely why China chose this lever to protect its own farmers.

European exposure is primarily industrial rather than agricultural. Producers like Yara carry diversified supply arrangements and EU purchasing power provides some buffer on spot markets. The more direct European vulnerability sits upstream: sulphuric acid consumers in the mining, chemicals, and battery materials sectors face the same constrained volumes as fertiliser producers, without the political insulation that food security arguments afford.

Copper and Silver

Chile is the most exposed nation in the metals complex. Its copper producers, such as Codelco, BHP, and Antofagasta Minerals, rely heavily on sulphuric acid for heap leaching and Solvent Extraction-Electrowinning (SX-EW) operations, the dominant processing method for low-grade copper ores. [2] [3] Without a replacement supply source, major Chilean mines face operational failure or Force Majeure declarations, which would permanently remove significant volumes of copper and its co-product silver from the 2026 global supply balance.

Indonesian Nickel and the Battery Metals Squeeze

Major Indonesian nickel producers such as PT Halmahera Persada Lygend, Zhejiang Huayou Cobalt, and Tsingshan Group-backed operations (including PT QMB New Energy Materials) are rapidly scaling Mixed Hydroxide Precipitate (MHP) production for the EV battery market. [9] MHP hydrometallurgy via high-pressure acid leaching (HPAL) is exceptionally sulphur-intensive. Crucially, these nickel producers will pay significant premiums to secure acid supply regardless of price, which means the battery sector is actively outbidding the more price-sensitive fertiliser industry for the same constrained volumes.

The Waste Streams That Become Strategic Assets

The crisis has accelerated serious attention toward three recovery technologies that were previously considered niche or marginally economic, enabling domestic sulphuric acid production and resilience.

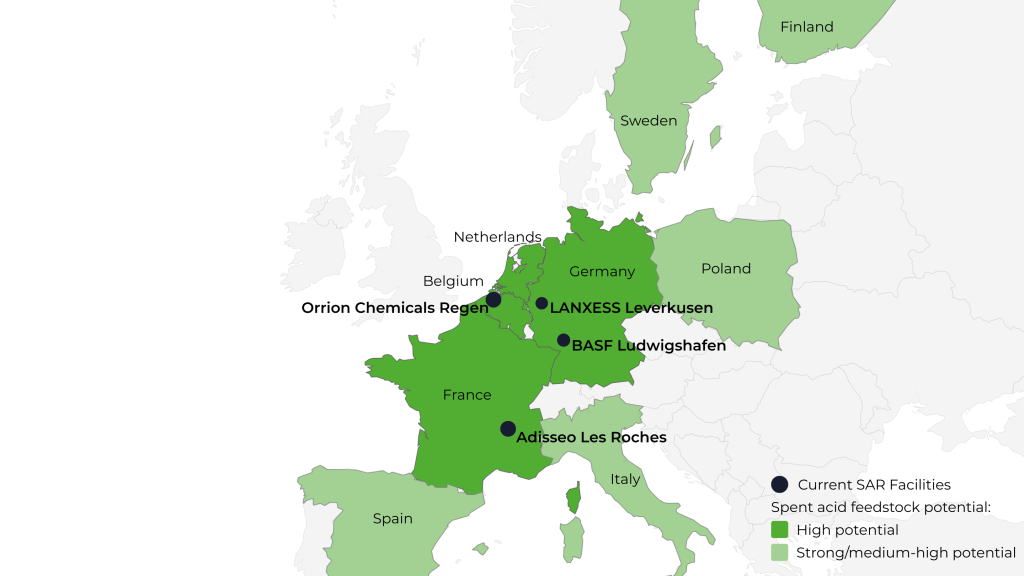

Spent Acid Regeneration (SAR). Petroleum refining and battery recycling generate large volumes of contaminated “spent” acid that still contains high sulphur concentrations. Regeneration units such as Adisseo’s Les Roches facility in France and LANXESS’s sulfuric acid plant in Leverkusen, Germany, restore spent acid to fresh sulfuric acid, closing the loop without primary elemental sulfur imports. [1] [8] This pathway already operates at an industrial scale in Europe and represents the most immediately scalable secondary supply option.

Phosphogypsum Valorisation. Phosphogypsum (PG) is the calcium sulphate waste generated during phosphoric acid production, one of the largest industrial waste streams globally. Two recovery routes are gaining traction: thermochemical decomposition, which uses reducing agents at high temperatures to release SO₂ for acid regeneration, and carbonation technology, which converts PG into calcium carbonate while recovering sulphur and capturing CO₂. The UNECE has flagged 100% utilisation of phosphogypsum as a strategic circular-economy target. [20]

Biodesulfurization (BDS). At the innovation frontier, microbial solutions are advancing toward commercial viability. The anaerobic bacterium Desulfovibrio desulfuricans can remove hydrogen sulphide from biogas and wastewater under ambient conditions. [12]

Europe: Between Policy Ambition and Market Reality

Europe’s refiners have shifted toward low-sulphur crudes from the US and Norway, reducing the sulphur available for domestic recovery.

The fundamental obstacle is economic. Circular recovery methods, like SAR, PG valorisation, and BDS, are energy-intensive processes. At current European energy prices, secondary materials frequently remain more expensive than primary imports from China or the Gulf. As Mario Draghi argued in his European competitiveness report, meaningful strategic autonomy in secondary raw materials may ultimately require carbon pricing that internalises the negative externalities of primary extraction to make domestic circular production cost-competitive. [7]

The ability to track secondary raw material inventories, phosphogypsum stack volumes, spent acid availability, and biodesulfurisation yields by region is moving from a technical niche to a core competitive intelligence requirement. Operators and investors who can map these secondary supply flows before a crisis will be positioned very differently from those who cannot. Get in touch with our team for further intelligence on global SAR and phosphogypsum availability and supply.

References

- Adisseo. (n.d.). Sulfuric acid and regeneration. https://www.adisseo.com/eu/products/sulfuric-acid

- Antofagasta plc. (2024). Annual report. https://www.aminerals.cl/docs/default-source/archivo/reportes/annual-report-2024.pdf

- BHP. (2024). Chilean copper site tour presentation. https://www.bhp.com/-/media/documents/media/reports-and-presentations/2024/241118_chilecoppersitetour_presentation.pdf

- Bloomberg News. (2026, April 10). China moves to ban sulfuric acid exports as Iran war hits supply. https://www.bloomberg.com/news/articles/2026-04-10/china-moves-to-ban-sulfuric-acid-exports-as-iran-war-hits-supply

- Canada Action. (2026, May 16). Sulphur in Canada: 10 facts & statistics. https://www.canadaaction.ca/sulphur-canada-facts

- Daly, T. (2026, April 22). Copper king Chile faces acid supply crunch as China exports dry up. Reuters. https://www.reuters.com/business/energy/copper-king-chile-faces-acid-supply-crunch-china-exports-dry-up-2026-04-22/

- Draghi, M. (2024). The future of European competitiveness: In-depth analysis and recommendations (Part B). European Commission. https://commission.europa.eu/topics/competitiveness/draghi-report_en#paragraph_47059

- LANXESS AG. (2019, September 19). One hundred and twenty-five years young – LANXESS sulfuric acid plant celebrates its birthday. https://lanxess.com/en/media/press-releases/2019/09/one-hundred-and-twenty-five-years-young-%E2%80%93-lanxess-sulfuric-acid-plant-celebrates-its-birthday

- Mining.com. (2026, April 14). Indonesia nickel makers trim battery-feed output as sulphur squeeze bites. https://www.mining.com/web/indonesia-nickel-makers-trim-battery-feed-output-as-sulphur-squeeze-bites/

- Nutrien Ltd. (2023). 2023 Fact Book. https://nutrien-prod-asset.s3.us-east-2.amazonaws.com/s3fs-public/uploads/2023-11/Nutrien_2023Fact%20Book_Update_112723.pdf

- OCP Group. (2021). Sustainability Integrated Report. https://ocpsiteprodsa.blob.core.windows.net/media/2022-08/OCP%20GROUP%20INTEGRATED%20REPORT%202021.pdf

- Papi, S., et al. (2018). Biological removal of gaseous sulfur dioxide through the reduction to hydrogen sulfide by means of Desulfovibrio desulfuricans. Process Safety and Environmental Protection. https://www.sciencedirect.com/science/article/abs/pii/S096483051730848X

- S&P Global Commodity Insights. (2026, March). Sulfur, nitrogen markets under pressure as Middle East war persists. https://www.spglobal.com/energy/en/news-research/latest-news/agriculture/031926-sulfur-nitrogen-markets-under-pressure-as-middle-east-war-persists-analysts

- SkyQuest Technology Consulting Pvt. Ltd. (2026). Sulfuric acid market size, share, growth | Report [2033]. https://www.skyquestt.com/report/sulfuric-acid-market

- SMM. (2025, December 29). [SMM analysis] Sulfur special series – Supply: Kazakhstan. https://news.metal.com/newscontent/103696006

- Sulphur Institute. (n.d.). Introduction to sulphur. https://www.sulphurinstitute.org/about-sulphur/introduction-to-sulphur/

- The Mosaic Company. (2024). Form 10-K. https://minedocs.com/28/Mosaic-Comp-Form-10-K-2024.pdf

- The Russian Government. (2026, March 31). Government extends temporary ban on exporting industrial sulfur. http://government.ru/en/docs/58223/

- U.S. Geological Survey. (2019). Sulfur (Mineral commodity summaries). https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-sulfur.pdf

- United Nations Economic Commission for Europe (UNECE). (2025, May 9). UNRMS and the road to 100% phosphogypsum utilization. https://unece.org/circular-economy/news/waste-opportunity-unrms-and-road-100-phosphogypsum-utilization