The 2026 Realignment: Circular and Biobased Solutions for a Fractured Supply Chain

Part 1: The Energy Pillar

The conflict that began in late February 2026 has produced an energy shock with no recent historical precedent. In a matter of weeks, the global energy system has been confronted with the simultaneous disruption of oil, natural gas, and critical material supply chains, all flowing through a single chokepoint: the Strait of Hormuz (Wood Mackenzie, 2026).

The Hormuz Chokepoint

Approximately 20 million barrels per day, 20% of the global oil supply, move through the Strait of Hormuz (U.S. Energy Information Administration, 2025). Bypass pipelines from Saudi Arabia and Iraq can reroute only 3.5-5.5 Mb/d. There is no alternative path for the remainder. For the gas market, the situation is even more acute: Qatar has no bypass route whatsoever. Every cubic meter of Qatari Liquid natural gas (LNG) must transit Hormuz.

The physical damage to supply infrastructure makes this more than a political standoff. Qatar’s Ras Laffan complex, the world’s largest LNG export facility, has sustained damage, reducing its capacity by approximately 17%. QatarEnergy has declared force majeure on all LNG exports. Repair estimates run from 3 to 5 years. That single hit removed approximately 12.8 million tonnes of LNG per year from global markets for the medium term (Wood Mackenzie, 2026). Iran’s South Pars field, the world’s largest natural gas deposit, has been severely damaged by strikes. Kharg Island, which accounts for over 90% of Iran’s oil exports, has been heavily hit.

Europe’s Storage Problem Has No Quick Fix

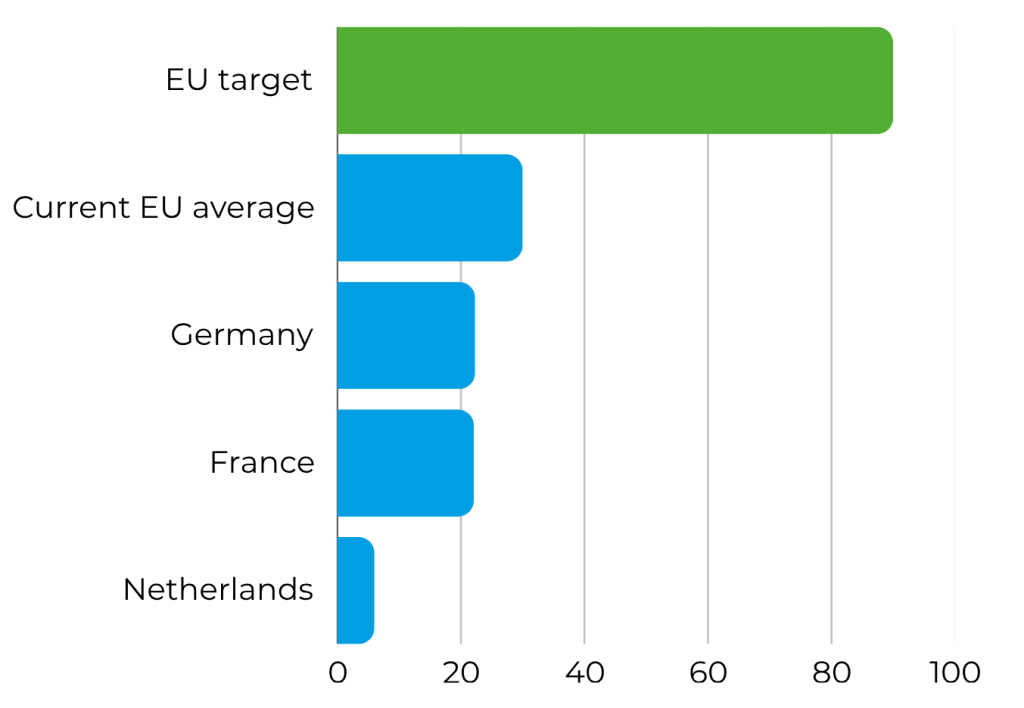

Time couldn’t be worse for the EU as its gas storage entered this crisis at 27–30% capacity, the lowest level for this point in the year since 2022 (Atlantic Council, 17 March 2026). Germany stands at 22.3%, France at 22.1%, and the Netherlands at just 6.0% (S&P Global, 2026). The EU requires approximately 60 billion cubic meters of injection before the next winter heating season to reach the 90% storage target (Atlantic Council, 17 March 2026). At current access rates and prices, the Atlantic Council assessed on 17 March that this is physically impossible, even if a ceasefire were agreed immediately.

The Atlantic Council’s assessment from 17 March 2026 is unambiguous: even in a ceasefire scenario, Europe is likely already heading toward an energy crisis. The question is not whether disruption will materialize, but how severe it will be and whether domestic alternatives can be scaled fast enough to matter.

Why This Creates a Structural Opportunity for Circular Energy

The traditional EU response to an energy crisis is to diversify import sources. In 2022, that meant replacing Russian pipeline gas with LNG from Qatar, the US, and Norway. That playbook does not work in 2026. The disruption is to the global LNG supply base itself and not to a single bilateral relationship.

This changes the terms of the conversation around circular and biobased energy. Biomethane, biofuels, and bio/e-methanol are not import-competing; they are import-independent. They are produced from domestic feedstocks by domestic operators and injected into existing infrastructure. They do not require new shipping routes, new geopolitical relationships, or new regasification capacity. And crucially: their economics have just shifted decisively.

The economics of the energy transition have flipped.

When fossil gas traded at €32–37/MWh and naphtha was cheap, circular alternatives carried a heavy premium. But when TTF prices surge above €60/MWh, as they have during this Hormuz disruption, biogas project economics improve dramatically, and bio-methanol shifts from a long-term sustainability play to a near-term procurement necessity (Atlantic Council, 17 March 2026). The disruption has not created the circular energy opportunity; rather, it has accelerated the timeline by years.

Closer Look at Available Domestic Circular Alternatives

01 — Biogas and Biomethane: The Domestic Gas Replacement

The EU currently produces approximately 22 billion cubic meters (bcm) of biogas and biomethane annually, of which 19 bcm originates within the EU-27 (European Biogas Association, 2025). To contextualize that scale: it is equivalent to the entire gas demand of Belgium, Denmark, and Ireland combined, yet only 6% of total EU gas consumption. Against a total EU consumption of 332 bcm (of which 273 bcm is still imported), the gap is obvious (European Biogas Association, 2025).

Biomethane is the fastest-growing segment of the European energy transition. In 2024, EU-27 biomethane production reached 5.2 bcm, up from 4.3 bcm the prior year. Europe now has 1,620 biomethane production facilities, 86% of which are grid-connected. By early 2025, installed capacity reached 7 bcm per year. Ahead of 2030, €28.4 billion in private investment has already been committed to biomethane development across Europe (European Biogas Association, 2025).

What Makes Biomethane Different from Every Other Alternative

The EU’s available gas alternatives (additional US LNG, Norwegian pipeline, Algerian supply) share a common limitation: they are all priced into the same global market that has just experienced its largest supply shock in history. Biomethane is not. It is produced from agricultural residues, food waste, sewage sludge, industrial organic by-products, and manure by domestic operators and injected directly into existing gas infrastructure.

The European Biogas Association projects that by 2040 the sector could produce up to 100 bcm annually, meeting an estimated 80% of EU gaseous fuel demand. Even the intermediate REPowerEU target of 35 bcm by 2030 would represent a 60% increase from today’s production (REPowerEU, 2026), and it is now a target underpinned by direct supply security logic rather than climate policy alone (European Biogas Association, 2025).

There is a second reason biomethane is uniquely positioned: its by-product. The digestate produced in biomethane plants is itself a circular fertiliser. In 2024, Europe generated 25 million tonnes of digestate (dry matter) (European Biogas Association, 2025). The EBA estimates that this material already has the potential to replace 17% of the EU’s nitrogen-based fertiliser consumption today — and could replace over 65% of non-renewable nitrogen by 2040 (European Biogas Association, 2024). A single biomethane value chain simultaneously addresses both the gas and fertiliser shortages: two of the three most acute crisis signals from this disruption. This will be examined in depth in the upcoming VCG.A.I.’s intelligence reports.

Where the Bottleneck Actually Is

The European Biogas Association’s 2025 statistical report identifies the primary barrier to faster biomethane deployment as neither technological nor financial, but rather problems of feedstock visibility and project coordination. Circular producers are sourcing from fragmented suppliers across member states, raising costs and slowing project development. The EU’s 2025 Bioeconomy Strategy explicitly acknowledges that there is no single EU market for secondary biomass, and that this fragmentation is the primary structural barrier to scaling.

The constraint is not technology. It is feedstock origination.

Projects stall because developers cannot efficiently identify, qualify, and secure the agricultural residues, food waste, and organic by-products that enable biomethane economics. This is the challenge that VCG.AI and similar data solutions are solving in real time: mapping feedstock availability, operators, and off-take partners across European markets, from before project development begins through long after it’s already running.

02 — Biofuels: Liquid Replacements Already at Commercial Scale

While biomethane addresses the gaseous fuel gap, liquid biofuels represent the second major energy pillar and one already operating at a significant commercial scale across Europe. The EU biofuel market was valued at $43.7 billion in 2025 and is projected to grow at a 9.4% CAGR through 2035 (Global Market Insights, 2026), reaching $62.8 billion by 2031. These are not pilot projects or policy aspirations, but rather operational industries subject to binding EU mandates.

HVO — Hydrotreated Vegetable Oil

HVO (Hydrotreated Vegetable Oil, also marketed as renewable diesel) is a drop-in replacement for fossil diesel: chemically identical, compatible with existing engines and infrastructure without blend limits. European HVO capacity reached approximately 10 million metric tonnes per year by 2025, doubling in two years (European Commission, 2026). Critically, since the war began, the price premium for HVO compared with fossil gasoil has fallen sharply as gasoil prices have surged. The economics of the switch have changed. BMW announced HVO100 as the standard initial fill for all diesels produced in Germany from January 2025. Major producers, including Neste, are operating near full capacity, with the next significant expansion scheduled for completion in 2027 at 2.7 million tonnes per year (Neste, 2025).

SAF — Sustainable Aviation Fuel

Sustainable Aviation Fuel entered mandatory blending territory in 2025 under the ReFuelEU Aviation regulation, with a 2% SAF obligation now in effect at all EU airports, rising to 50% by 2050 (REPowerEU, 2026). Aviation is the transport sector that cannot be electrified on any viable timeline, leaving SAF as the only decarbonization pathway. SAF production is expected to account for nearly one quarter of all hydrotreating capacity additions in Europe between 2026 and 2031, permanently altering refinery economics. TotalEnergies shifted 40% of its La Mède refinery output to jet fuel in 2024. The mandate means that SAF feedstock intelligence has become a commercial priority for every European airline and refinery independently of the current disruption.

Bioethanol

EU bioethanol production hit a record high of 5.70 billion liters in 2025 (USDA Foreign Agricultural Service, 2025), with further growth expected. Bioethanol functions both as a direct fuel blending component (E10 is now the standard across most of Europe) and as an approved SAF feedstock via the alcohol-to-jet (ATJ) pathway, estimated to produce 3.5 million metric tonnes of SAF by 2030, rising to 5.8 million tonnes by 2050.

The European Commission’s own research, published in February 2026, confirms that with financial and administrative support, domestic production of advanced biofuels can be scaled to 14.4 Mtoe by 2030 (European Commission, 2026) — a multi-fold increase from current levels. The constraint, again, is not technology. It is feedstock origination and project development speed.

03 — Bio-Methanol and e-Methanol: Fuel and Feedstock in One

Methanol occupies a unique position in the current disruption because it is simultaneously a fuel and a chemical feedstock. As a fuel, it is the primary candidate for maritime decarbonization. The shipping sector, which cannot electrify at scale, is investing heavily in methanol-powered vessels. As a feedstock, it is the upstream input for formaldehyde, acetic acid, MTBE, synthetic resins, solvents, and a broad range of polymer derivatives. These applications will be examined in depth in the upcoming VCG.A.I.’s intelligence reports. For the energy pillar, the fuel dimension is the most immediate story.

Today, more than 100 million tonnes of methanol are produced annually using natural gas and coal (NETL, n.d.; Statista/Methanol Institute, 2022). The Gulf, via natural gas, is a primary production base. That supply is now disrupted. Force majeure has been declared on methanol exports from Gulf facilities, and the downstream impact is already being felt across chemical value chains.

The Renewable Methanol Scale-Up

The renewable methanol market is scaling faster than almost any other biobased sector. In 2026, renewable methanol capacity is projected to reach approximately 2 million tonnes (GENA Solutions/Bioenergy International, 2026). Eight commercial-scale projects reached final investment decisions during 2025 alone. Europe is the fastest-growing regional market, at a projected 47.87% CAGR, driven primarily by maritime decarbonization mandates under FuelEU Maritime (Research and Markets, 2025).

The most concrete operational example is the Kassø facility in Denmark, operated by European Energy (European Energy, 2025). It is the world’s first large-scale e-methanol production site, producing up to 42,000 tonnes of e-methanol per year. It already supplies Maersk’s first methanol-powered container vessel and serves LEGO and Novo Nordisk as a substitute for fossil plastic feedstock. The next generation of plants, using electrified steam methane reforming of biomethane, is scheduled for commercial operation in 2029 at 100,000+ tonnes per year per facility.

The Kassø e-methanol facility in Denmark.

(Source: European Energy)

For chemical and petrochemical producers specifically, renewable methanol is a direct drop-in replacement for fossil methanol in most applications. Chemical and petrochemical producers controlled 35.2% of renewable methanol end-user demand in 2025 (FactMR, 2026). As Gulf methanol supply contracts and prices surge, switching to domestically produced bio-methanol or e-methanol has shifted from a long-term sustainability objective to a near-term procurement necessity.

The Common Thread

Across all three energy sub-pillars (biomethane, biofuels, and bio/e-methanol), the same core constraint surfaces. The technology exists. The policy frameworks are in place. European industrial capacity is mobilising. What is missing is integrated intelligence around feedstock, technologies, and markets. Intelligence that can leverage the existing capacity to the fullest and ensure that a successful scale-up, based on the resources available in Europe, can be executed at the right places at the right time.

Agricultural residues, food processing waste, used cooking oils, sewage sludge, woody biomass: these are the inputs that determine whether a biomethane plant gets built, whether an HVO refinery can run at capacity, and whether an e-methanol facility secures its carbon feedstock. They are geographically distributed, volume-variable, compositionally diverse, and operating under member-state regulatory frameworks that are not yet harmonised.

This is not a problem that yields to more policy or more capital. It yields to better information. Granular, cross-border, primary-data intelligence on feedstock availability, operator capacity, and off-take markets, maintained in real time as the disruption continues to evolve.

That intelligence gap is what VCG.AI is built around. Mapping exactly this landscape: feedstock flows, qualified operators, and off-take partners across European and global markets. In a disruption of this scale and speed, the companies that close that information gap first will not just manage risk better, but they will find opportunities their competitors cannot yet see.

References:

Atlantic Council. (2026, March 17). How the Iran war could trigger a European energy crisis.https://www.atlanticcouncil.org/dispatches/how-the-iran-war-could-trigger-a-european-energy-crisis/

European Biogas Association. (2024). Exploring digestate’s contribution to healthy soils.https://www.europeanbiogas.eu/wp-content/uploads/2024/03/Exploring-digestate-contribution-to-health-soils_EBA-Report.pdf

European Biogas Association. (2025). EBA statistical report 2025. https://www.europeanbiogas.eu/news/eba-statistical-report-2025/

European Commission. (2026, February 2). A multi-fold increase in advanced biofuel industrial capacity possible by 2030. https://research-and-innovation.ec.europa.eu/news/all-research-and-innovation-news/multi-fold-increase-advanced-biofuel-industrial-capacity-possible-2030-2026-02-02_en

European Commission. (n.d.). REPowerEU: Phase out of Russian energy imports. Retrieved March 30, 2026, from https://energy.ec.europa.eu/strategy/repowereu-phase-out-russian-energy-imports_en

European Energy. (2025). Kassø e-methanol facility. https://europeanenergy.com/kasso/

FactMR. (2026). Renewable methanol market: Global market analysis report 2036.https://www.factmr.com/report/renewable-methanol-market

GENA Solutions Oy & Methanol Institute. (2026, January 28). 2025 a watershed year for renewable and low-carbon methanol projects. Bioenergy International. https://bioenergyinternational.com/2025-a-watershed-year-for-renewable-and-low-carbon-methanol-projects/

Global Market Insights. (2026). Europe biofuel market size, 2026–2035 forecast. https://www.gminsights.com/industry-analysis/europe-biofuel-market

Methanol Institute. (2022). Production of methanol worldwide from 2017 to 2022 [Graph]. Statista. https://www.statista.com/statistics/1323406/methanol-production-worldwide/

Neste. (2025, April 9). Neste started producing sustainable aviation fuel (SAF) at its renewables refinery in Rotterdam. https://www.neste.com/news/neste-started-producing-sustainable-aviation-fuel-saf-at-its-renewables-refinery-in-rotterdam-the-netherlands

Research and Markets. (2025). Europe renewable methanol market forecast 2024–2038.https://www.researchandmarkets.com/report/europe-renewable-methanol-market

Resourcewise. (2026, March). Despite energy uncertainty, optimism persists in European biofuels.https://www.resourcewise.com/blog/despite-energy-uncertainty-optimism-persists-in-european-biofuels

S&P Global. (2026, March 31). FEATURE: Low gas storage, LNG disruption to test European resilience. https://www.spglobal.com/energy/en/news-research/latest-news/natural-gas/033126-feature-low-gas-storage-lng-disruption-to-test-european-resilience-in-q2

U.S. Department of Energy, National Energy Technology Laboratory. (n.d.). Syngas conversion to methanol.https://netl.doe.gov/research/carbon-management/energy-systems/gasification/gasifipedia/methanol

U.S. Energy Information Administration. (2025, February). Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint. https://www.eia.gov/todayinenergy/detail.php?id=65504

USDA Foreign Agricultural Service. (2025). Biofuels annual – European Union.https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Biofuels+Annual_The+Hague_European+Union_E42025-0004.pdf

VCG.AI. (2026). VCG.AI Intelligence Platform. VCG.AI. https://vcg.ai

Wood Mackenzie. (2026, March 30). Strait of Hormuz blockade bites global chemicals sector.https://www.woodmac.com/news/opinion/strait-of-hormuz-blockade-bites-global-chemicals-sector/