The 2026 Realignment: Circular and Biobased Solutions for a Fractured Supply Chain

Part 3: Fertilisers Pillar

The first two parts of this series tracked the shock across energy markets and petrochemical feedstocks. Biomethane, HVO, and SAF shifted from long-term sustainability plays to near-term supply security instruments. Biobased chemistry moved from an ambition to a procurement question. The structural logic was consistent: domestic circular production chains, constrained not by technology readiness but by feedstock visibility, now hold measurable advantages over fossil-dependent import flows.

Fertilisers complete the picture. And in some ways, they complicate it.

The Numbers

Urea is up 50–77%. Ammonia is up 20–25%. Sulfur is up 50%.

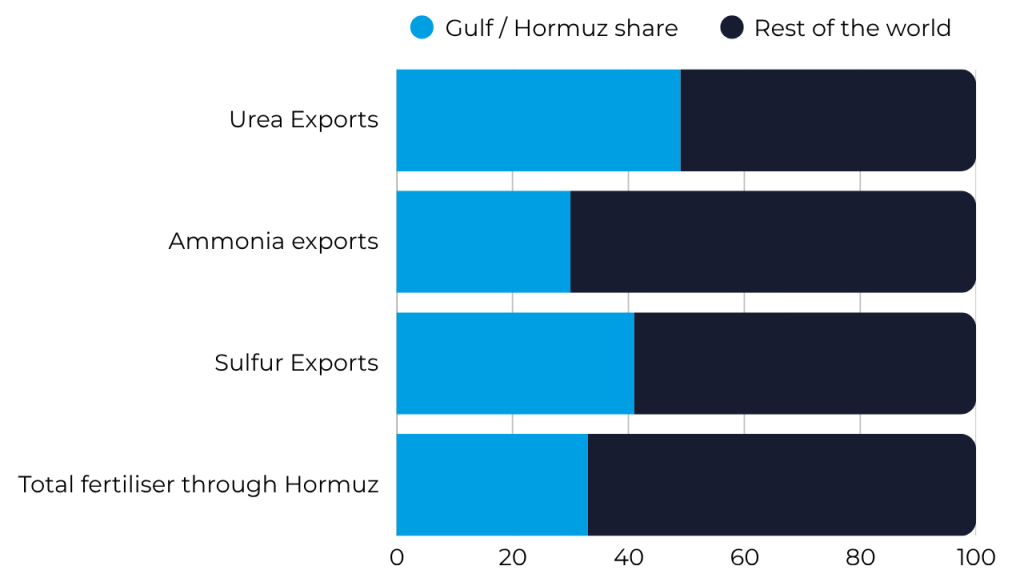

20-30% of global fertiliser exports transit the Strait of Hormuz. Gulf states supply approximately 43% of global urea, 25% of traded ammonia, and 50% of globally traded sulfur. [1] Unlike oil, there are no strategic fertiliser reserves. Unlike gas, there is no spot LNG cargo that can be redirected on short notice. And unlike chemicals, the downstream consequences of a fertiliser shortage do not show up in an industrial margin, but rather in crop yields, six to twelve months later.

Spring planting has already begun across most of the Northern Hemisphere.

Ethiopia receives over 90% of its nitrogen fertiliser from the Gulf. In India, major producers, including IFFCO, have been forced to reduce output as LNG supplies were cut by up to 40%. [7] The FAO has warned that the disruption threatens to halve crop yields in affected regions, potentially pushing 45 million additional people into acute hunger by June 2026. [2]

The price and production signal are real. The lag before it becomes a food signal is the only reason it has not yet dominated the news cycle.

The Structural Problem: Haber-Bosch as a Gas Derivative

The reason fertiliser prices track gas prices is not incidental. It is chemical. At its core, the Haber-Bosch process combines atmospheric nitrogen with hydrogen under high pressure and temperature to synthesise ammonia: the base compound for virtually all nitrogen fertilisers.

The process accounts for more than 90% of global ammonia synthesis, consuming approximately 6.4 × 10¹² MJ of non-renewable energy annually and emitting roughly 1.5 tonnes of CO₂ per tonne of ammonia produced. [3] The hydrogen used in the process is produced by steam-methane reforming of natural gas. Ammonia is, structurally, a gas derivative with extra steps.

This means the fertiliser shortage is not a secondary consequence of the Hormuz disruption but a direct one. In the EU, producers reliant on spot TTF prices, which have now roughly doubled, face the same mathematics: when gas approaches €70/MWh, ammonia synthesis at several facilities becomes unviable before the logistics question even arises.

The fix is not a supply chain fix. Rerouting shipping does not change what the process runs on. So long as Haber-Bosch is the production mechanism and natural gas is the feedstock, fertiliser prices will remain a function of gas prices and gas prices will remain a function of events in the Gulf.

What Circular Nitrogen Recovery Actually Offers

Europe generates approximately 180 million tonnes of anaerobic digestate per year from its 18,000+ biogas plants. [4] This digestate carries 2–5 kg/m³ of nitrogen and 0.5–1.5 kg/m³ of phosphorus, precisely the nutrients that conventional fertilisers supply. The technologies to recover these nutrients and convert them into marketable fertiliser products are not in development. They are commercially operational today.

Two primary routes dominate current deployment:

Ammonia stripping removes ammonium from liquid digestate and concentrates it into a recoverable ammonium salt. Field trials across Germany and the Netherlands show that recovered ammonium salts perform at 95–105% of the effectiveness of synthetic fertiliser. [5]

Struvite crystallisation precipitates magnesium ammonium phosphate from nutrient-rich effluents. Struvite performs as an effective slow-release fertiliser with lower heavy metal contamination profiles than conventional phosphate products and agronomic performance comparable to synthetic equivalents. [5]

Combined systems achieve phosphorus recovery above 90% and nitrogen recovery above 60% from liquid effluents. Under normal market conditions, recovered fertilisers from wastewater and digestate systems have been assessed to cost 20–30% less than synthetic equivalents. [5] Under current spot prices, that gap has widened considerably.

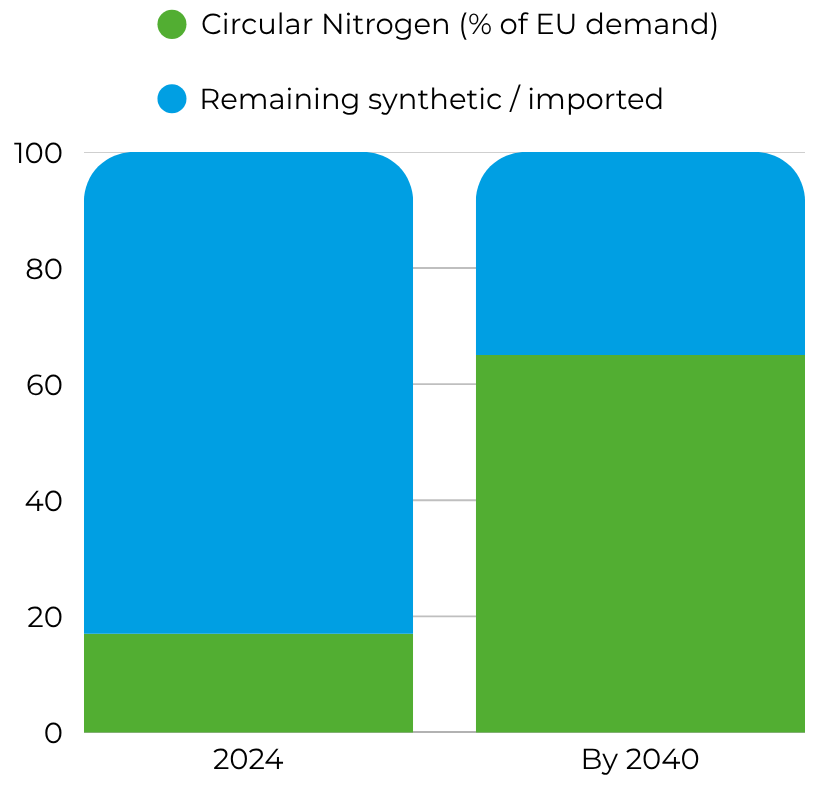

The European Biogas Association’s 2024 data quantifies the scale directly: the 25 million tonnes of digestate produced across the EU in 2024 already has the potential to replace 17% of EU nitrogen-based fertiliser consumption. [4] With the sector’s projected growth toward 100 bcm of biogas by 2040, digestate output scales proportionally, potentially enabling a 65%+ substitution of non-renewable nitrogen in the EU by mid-century. [4]

One figure from Part I of this series bears repeating here in a different context: biomethane’s by-product already addresses two of the three most acute crisis signals from the opening analysis. A single circular value chain, agricultural residues into biomethane, simultaneously reduces gas import dependency and produces domestically sourced fertiliser feedstock. That overlap is the underlying logic of circular production.

The Same Bottleneck, a Different Consequence

The pattern that defined the biomethane analysis in Part I and the biobased chemicals analysis in Part II reappears here: the binding constraint is not technology; it is feedstock market fragmentation.

Circular fertiliser producers are sourcing from heterogeneous waste streams with variable composition, inconsistent volumes, and regulatory frameworks that differ across member states on what constitutes waste, what constitutes a product, and what permits apply to land application of recovered nutrients. The EU’s 2025 Bioeconomy Strategy explicitly identifies the absence of a single EU market for secondary biomass as the primary structural barrier to scaling. [6] The Circular Economy Act, scheduled for adoption in 2026, aims to establish EU-wide end-of-waste criteria that would begin to dissolve this fragmentation. Until it does, the legal patchwork is both a constraint and, for operators who navigate it, a moat.

But the consequences of the bottleneck differ here from those in the energy and chemical pillars. In biofuels, fragmented feedstock origination delays scale-up, primarily with economic implications. In biobased chemicals, it slows the substitution of disrupted naphtha-derived inputs. In circular fertilisers, the downstream is food production. The fallback is not a more expensive polymer or a more expensive fuel blend. In some markets, there is no fallback.

That distinction matters for how urgently the intelligence gap is resolved and who resolves it first.

The Full Realignment

Three disruptions. Three value chains: gas, chemicals, fertilisers. One underlying structure: consolidated exposure to a single geopolitical corridor, built over decades on the assumption that the economics of concentration were stable.

Part I of this series showed that the energy transition’s circular alternatives were technically ready before the crisis; the crisis changed the economics. Part II showed the same was true of biobased chemistry. Part III shows the same in fertilisers, with the additional dimension that the cost of delay here is measured differently than in the other two pillars.

What is true across all three is this: the intelligence layer, knowing where the feedstocks are, who the qualified operators are, which projects are development-ready and which are stranded in the mapping gap, is the rate-limiting factor on how fast the transition actually moves. The technology is not waiting. The policy frameworks are moving. The capital is available. The constraints are origination and counterparty intelligence, and neither is resolving on its own.

References

[1] The Fertilizer Institute. (2026, March). Fertilizer and the Middle East conflict. https://www.tfi.org/wp-content/uploads/2026/03/Fertilizer-and-the-Middle-East-Conflict-2.pdf

[2] World Food Programme. (2026, March). WFP projects food insecurity could reach record levels as result of Middle East escalation. https://www.wfp.org/news/wfp-projects-food-insecurity-could-reach-record-levels-result-middle-east-escalation

[3] Smil, V. (2001). Enriching the earth: Fritz Haber, Carl Bosch, and the transformation of world food production. MIT Press.

[4] European Biogas Association. (2025, December 10). EBA statistical report 2025. https://www.europeanbiogas.eu/news/eba-statistical-report-2025/

[5] Lorick, D., Macura, B., Ahlström, M., Grimvall, A., & Harder, R. (2020). Effectiveness of struvite precipitation and ammonia stripping for recovery of phosphorus and nitrogen from anaerobic digestate: A systematic review. Environmental Evidence, 9(1), Article 27. https://doi.org/10.1186/s13750-020-00211-x

[6] European Commission. (2025, November 27). A strategic framework for a competitive and sustainable EU bioeconomy (COM/2025/960 final). https://environment.ec.europa.eu/document/download/dbf8d2ba-9332-4f7a-b336-f356fa4b7236_en?filename=COM_2025_960_1_EN_ACT_part1_v10_0.pdf

[7]Outlook Business. (2026, March 11). India’s fertilizer plants shut down as West Asia war cuts LNG supplies. https://www.outlookbusiness.com/economy-and-policy/indias-fertilizer-plants-shut-down-as-west-asia-war-cuts-lng-supplies